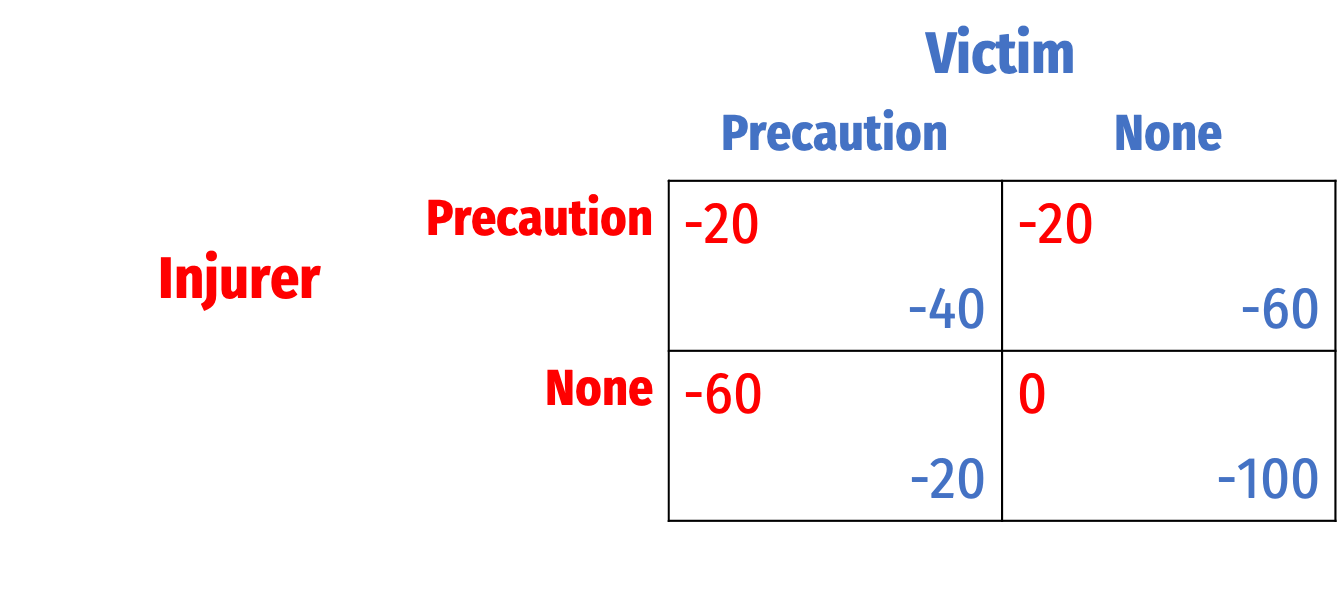

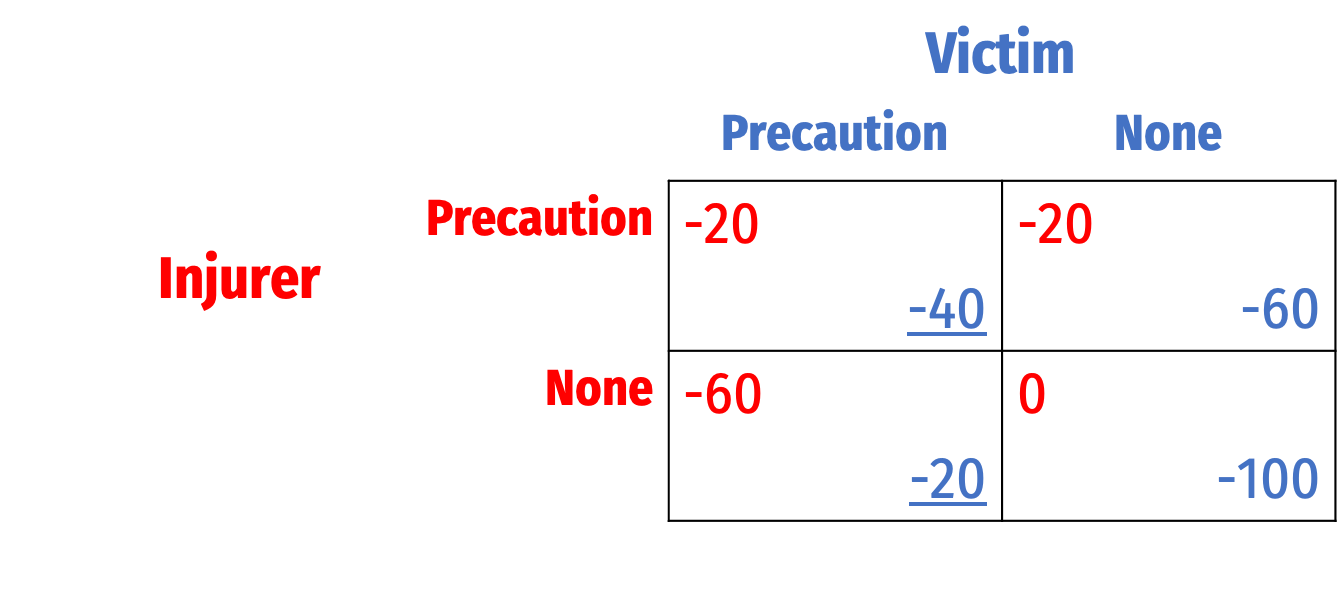

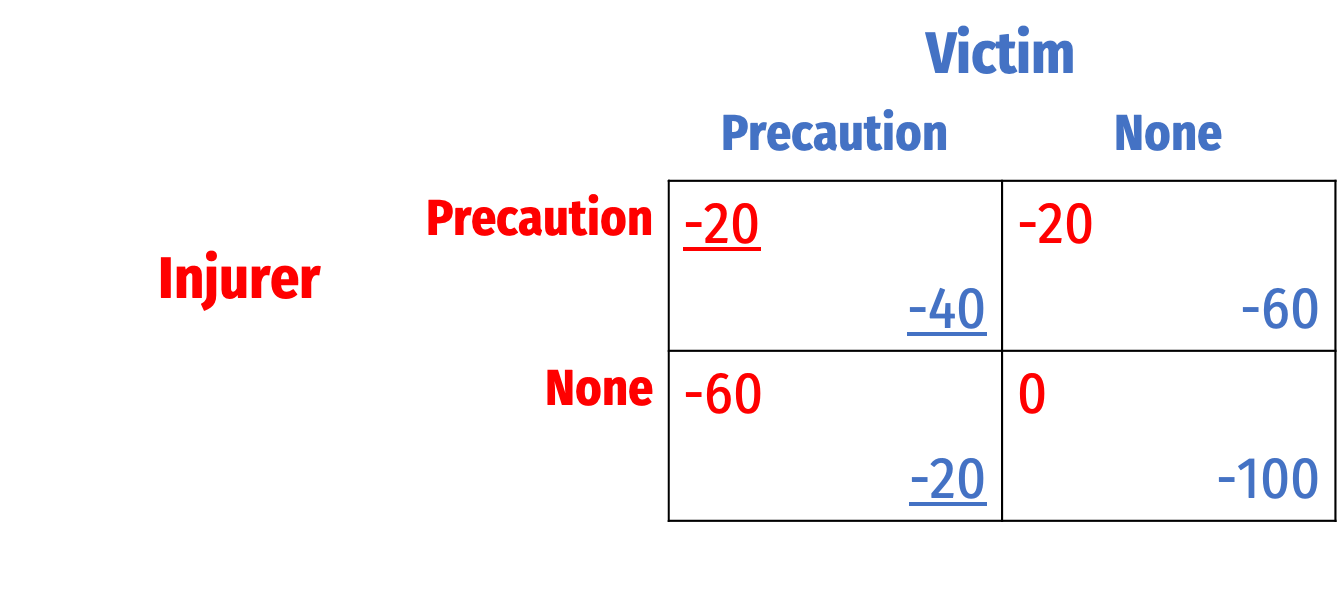

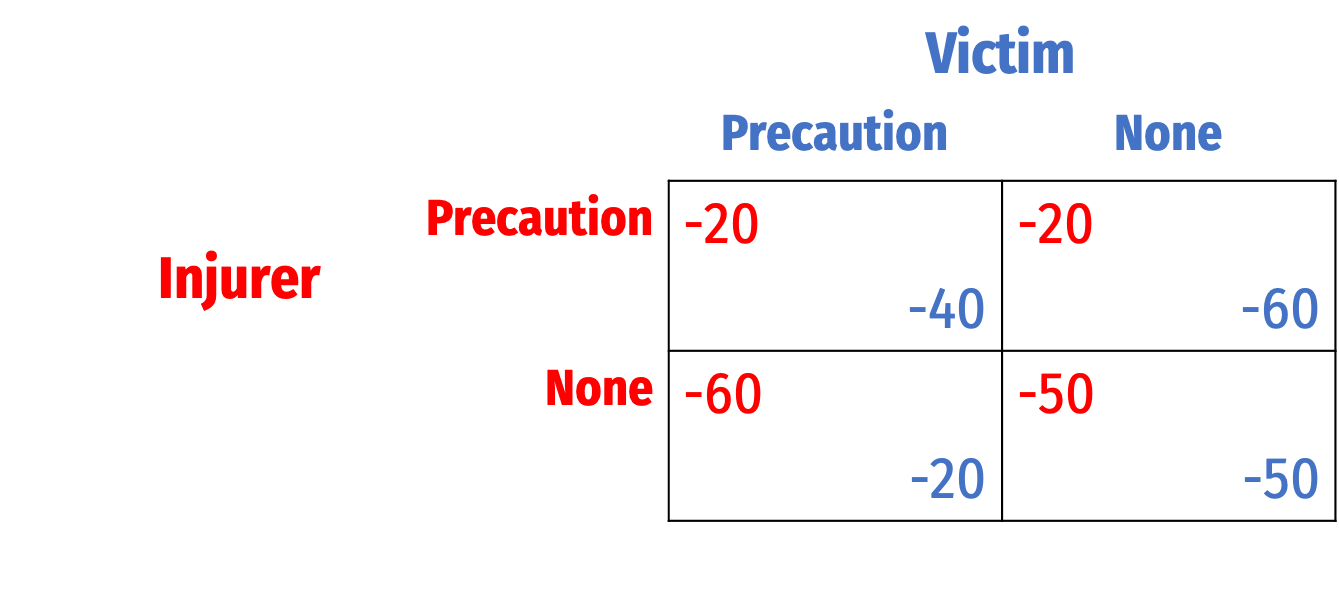

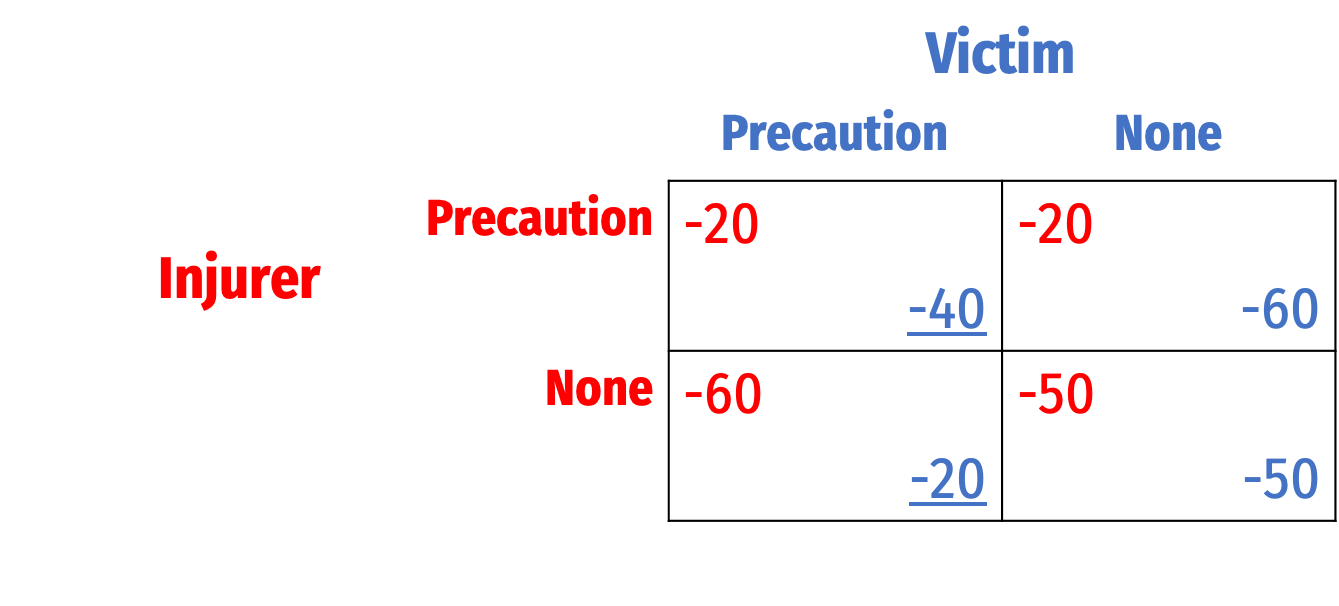

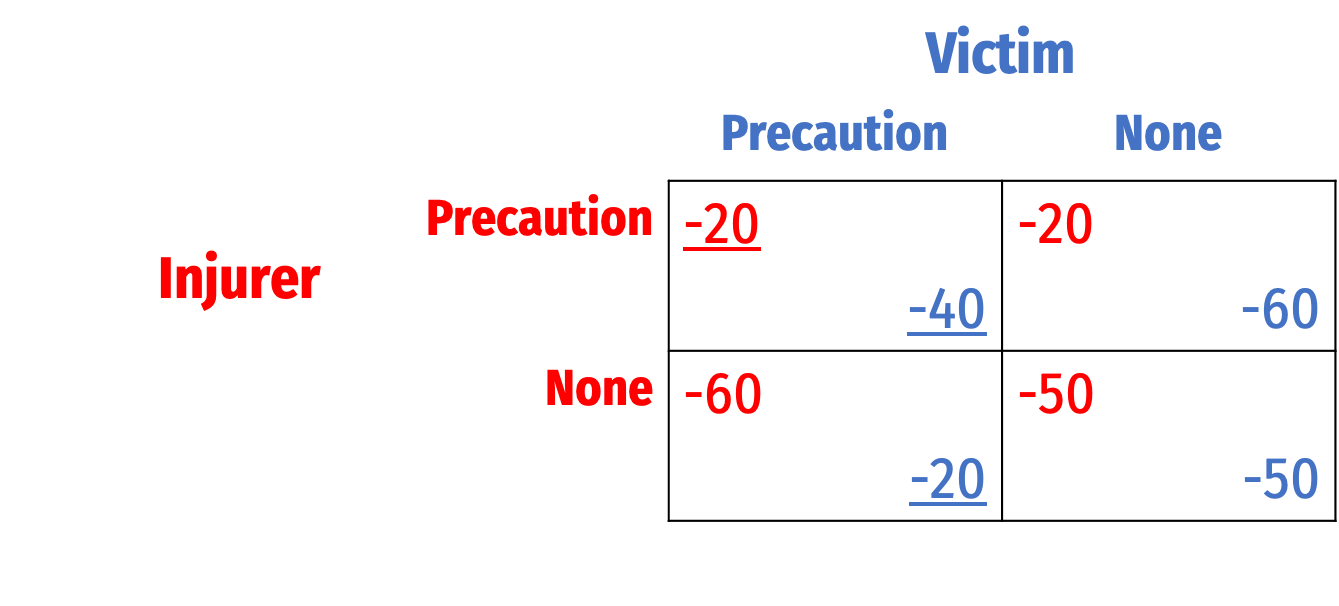

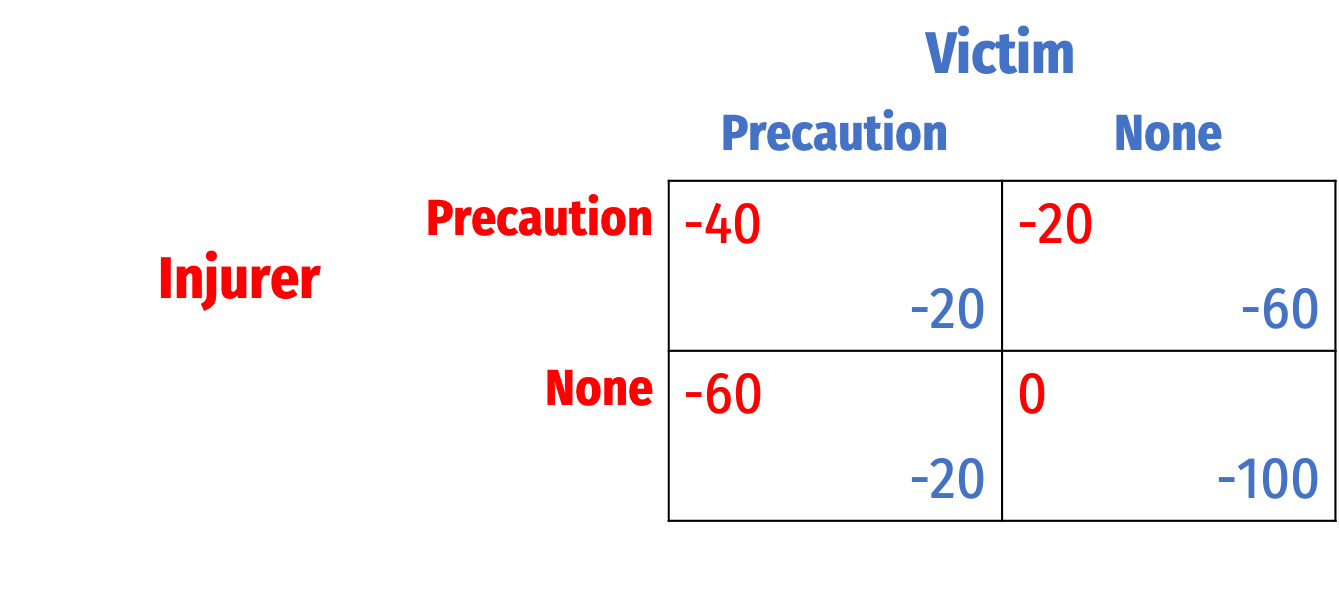

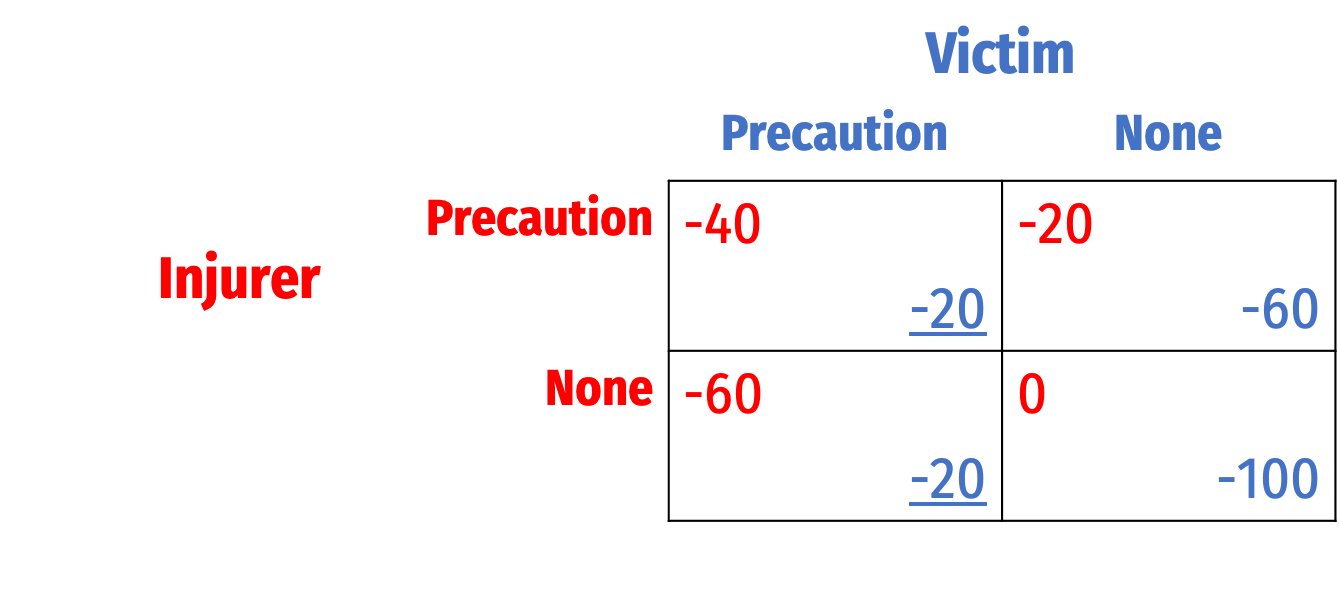

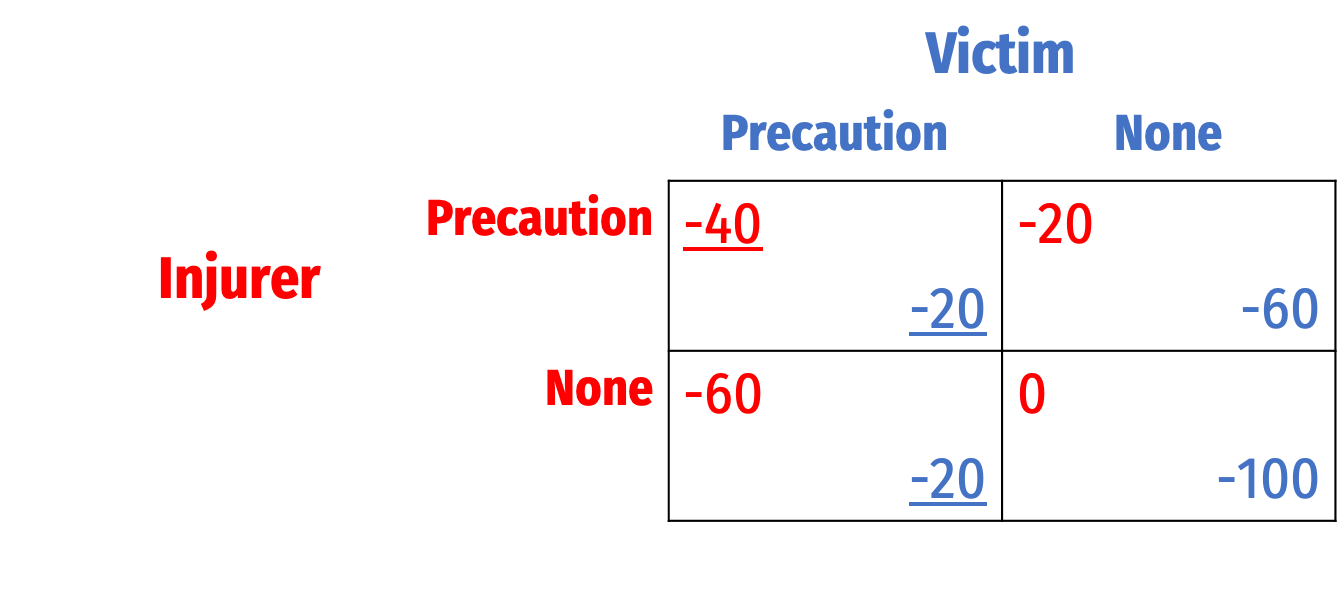

class: center, middle, inverse, title-slide # 4.2 — An Economic Model of Precaution ## ECON 315 • Economics of the Law • Spring 2021 ### Ryan Safner<br> Assistant Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/lawS21"><i class="fa fa-github fa-fw"></i>ryansafner/lawS21</a><br> <a href="https://lawS21.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>lawS21.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Precaution: An Economic Model](#3) ### [No Liability](#) ### [Strict Liability](#) ### [Negligence](#) ### [A Family of Negligence Rules](#) ### [Comparing Negligence Rules, A Discrete Example of Bilateral Caution](#) --- class: inverse, center, middle # Precaution: An Economic Model --- # Precaution .pull-left[ .smallest[ - As usual, our main concern is with the incentives these various liability rules create - For torts, focus on parties' incentive to invest in (costly) precaution to avoid accidents - Driving/bicyling carefully, installing seatbelts, airbags, wearing helmets, etc. - Inspecting products carefully, quality control, independent audits, mandatory work breaks - All of these things are **costly** to parties, so there must be some **efficient** level ] ] .pull-right[ .center[  ] ] --- # Precaution .smallest[ - Actions by both injurer and victim impact the number of accidents .pull-left[ - Speed like hell, drive drunk, texting - Bicycle in the dark wearing black, no helmet - Manufacture cheap, shoddy product quickly ] .pull-right[ - Drive slowly and soberly - Bicycle wearing helmet and reflectors - Manufacture slow, quality controlled & inspected product ] ] .center[  ] -- .smallest[ - .hi[Precaution]: any activity either party can do to reduce probability of an accident (or severity of damage) - .hi-purple[How much precaution is efficient?] - .hi-purple[How do we design the law to get this amount?] ] --- # A Simple Economic Model of Accidents .pull-left[ .smallest[ - Our main example was a car hitting a bicyclist, in real life: - Driver probably has insurance - Some damage to bicycle and to driver’s car - Driver and bicyclist may not even know what the law is - We will simplify a lot by assuming: - Only one party is harmed - Parties know the law - Parties don’t have any insurance (for now) - Focus only on one party’s precaution at a time ] ] .pull-right[ .center[  ] ] --- # A Unilateral Care Model .pull-left[ - Unilateral harm (just one victim) - .hi[Precaution]: costly actions that make accident less likely - Could be taken by either .blue[victim] or .red[injurer] - We'll consider both, but one at a time .center[  ] ] --- # A Unilateral Care Model: Definitions/Notation .pull-left[ .smallest[ - `\(x\)`: amount of precaution taken - `\(w\)`: cost of each “unit” or precaution - total cost of precaution is `\(wx\)` - `\(p(x)\)`: probability of an accident, given level of `\(x\)` - `\(\frac{\partial p(x)}{\partial x} < 0\)` - `\(A\)`: cost of accident (to victim) - expected cost of accidents is `\(p(x)A\)` - When we examine .red[injurer] we will use `\(x\)`, when we examine .blue[victim] we will use `\(y\)` - Your textbook uses `\(x^i\)` and `\(x^v\)` ] ] .pull-right[ .center[  ] ] --- # A Unilateral Care Model .pull-left[ - .green[Cost of precaution, `\\(wx\\)`] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-1-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model .pull-left[ - .green[Cost of precaution, `\\(wx\\)`] - .red[Cost of accidents, `\\(p(x)A\\)`] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-2-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model .pull-left[ - .green[Cost of precaution, `\\(wx\\)`] - .red[Cost of accidents, `\\(p(x)A\\)`] - .blue[Total Social Cost `\\(p(x)A+wx\\)`] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-3-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model .pull-left[ - .green[Cost of precaution, `\\(wx\\)`] - .red[Cost of accidents, `\\(p(x)A\\)`] - .blue[Total Social Cost `\\(p(x)A+wx\\)`] - Efficient level of precaution: `$$\min_{x} \ color{blue}{p(x)A+wx}$$` ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-4-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model .pull-left[ - .green[Cost of precaution, `\\(wx\\)`] - .red[Cost of accidents, `\\(p(x)A\\)`] - .blue[Total Social Cost `\\(p(x)A+wx\\)`] - Efficient level of precaution: `$$\min_{x} \color{blue}{p(x)A+wx}$$` - Optimum `\(x^\star\)`: .smallest[ `$$\begin{align*} \color{green}{w} &= \color{red}{-p’(x)A}\\ \color{green}{\text{MSC of precaution}} &= \color{red}{\text{MSB of precaution}}\\ \end{align*}$$` ] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-5-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model .pull-left[ - The efficient level of precaution, `\(x^\star\)` minimizes .blue[total social cost] - Balances the tradeoff between the .red[benefit of reduced accident likelihood] and the .green[cost of increased precaution] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-6-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model: Technical Note .pull-left[ .smallest[ - We are thinking of bilateral precaution, just “one party at a time”; again: - `\(x\)` represent level of precaution by .red[injurer] - `\(y\)` represent level of precaution by .blue[victim] - Really, the social problem between both parties: `$$\min_{x,y} p(x,y)A-wx-wy$$` ] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-7-1.png" width="504" style="display: block; margin: auto;" /> ] --- # A Unilateral Care Model: Technical Note .pull-left[ .smallest[ - “Hold fixed” one party’s solution and consider the other, e.g. `$$\min_x p(x,y)A-wx-wy \quad \text{ given y}$$` which has same solution as `$$\min_x p(x)A-wx$$` - Results will generally be efficient *given* what the other party is doing ] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-8-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Effect of Liability Rules on Precaution .pull-left[ - We know the **efficient** level of precaution is `\(x^\star\)`, which minimizes total social cost - Now let’s consider the effect of .hi-turquoise[different liability rules] have on the **chosen** amount of precaution ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # No Liability --- # No Liability .pull-left[ .smallest[ - Imagine a world of .hi[no liability] (NL) - .red[Injurer] pays nothing for accidents - Bears the .green[cost] of his precaution - But no .red[benefit] (of avoided damages) - **Has no incentive to take any precaution** - .blue[Victim] bears cost of any accidents, plus cost of her precaution taken - .blue[Victim] precaution imposes no externality on .red[Injurer] - .blue[Victim] will invest in efficient amount of precaution `\(y^\star\)` ] ] .pull-right[ .center[  ] ] --- # No Liability .pull-left[ - .red[Injurer]'s private costs: `\(\color{green}{wx}\)` `$$\min_{x} \color{green}{wx} \implies x_{NL}=0$$` ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-9-1.png" width="504" style="display: block; margin: auto;" /> ] --- # No Liability .pull-left[ - .red[Injurer]'s private costs: `\(\color{green}{wx}\)` `$$\min_{x} \color{green}{wx} \implies x_{NL}=0$$` - .blue[Victim]'s private costs: `\(\color{blue}{p(y)A+wy}\)` `$$\min_{y} \color{blue}{p(y)A+wy} \implies y_{NL}=y^\star$$` - chooses efficient precaution - Rule of .hi[no liability] leads to: - efficient precaution by .blue[Victims] - no precaution by .red[Injurers] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-10-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | |------|---------|--------| | No liability | Zero | .green[Efficient] | --- # Determining Accidents .pull-left[ - Precaution isn't the only thing that affects the number of accidents - Precautions are extra actions that make our activity less dangerous - Also the .hi-purple[amount of activities] we do affects the number of accidents - I decide how often to drive - You decide how often to bike - Liability rules also create incentives for .hi-purple[activity levels] ] .pull-right[ .center[  ] ] --- # Determining Accidents: No Liability .pull-left[ - With .hi[no liability], I am not liable if I hit you - I don't consider cost of accident when I decide **how fast** to drive - nor when I decide **how much** to drive - .hi-purple[So I drive too recklessly *and* too often] - My driving imposes a negative externality on others - With no liability, .red[Injurer]'s activity level is inefficiently high ] .pull-right[ .center[  ] ] --- # Determining Accidents: No Liability .pull-left[ - With .i[no liability], you bear the full cost of an accident - More activity by victim (bicycling) leads to more accidents - You weigh cost of accidents when deciding **how carefully** to ride, and **how much** to ride - Your private cost equals the social cost - .hi-purple[You take the efficient level of precaution, and efficient level of activity] ] .pull-right[ .center[  ] ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] --- class: inverse, center, middle # Strict Liability --- # Strict Liability .pull-left[ .smallest[ - Imagine a world of .hi[strict liability] (SL) with perfect compensation - `\(D=A\)` damages equal to the cost of the accident - .red[Injurer] pays for any accidents he causes - Bears the full .red[cost of accidents] plus his .green[precautions] taken - Receives .red[benefit] (of avoided damages) - Internalizes externality his actions cause, chooses the efficient level of precaution - .blue[Victim] is fully insured - Has **no incentive** to invest in any precaution ] ] .pull-right[ .center[  ] ] --- # Strict Liability .pull-left[ - .red[Injurer]'s private costs: `\(\color{blue}{p(x)A+wx}\)` `$$\min_{x} \color{blue}{p(x)A+wx} \implies x_{SL}=x^\star$$` - chooses efficient precaution ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-11-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Strict Liability .pull-left[ - .red[Injurer]'s private costs: `\(\color{blue}{p(x)A+wx}\)` `$$\min_{x} \color{blue}{p(x)A+wx} \implies x_{SL}=x^\star$$` - chooses efficient precaution - .blue[Victim]'s private costs: `\(\color{green}{wy}\)` `$$\min_{y} \color{green}{wy} \implies y_{SL}=0$$` - Rule of .hi[strict liability] leads to: - efficient precaution by .red[Injurers] - no precaution by .blue[Victims] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-12-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | |------|---------|--------| | No liability | Zero | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | --- # Strict Liability: Activity Levels .pull-left[ .smallest[ - Under strict liability, .red[injurer] internalizes cost of accidents - Weighs benefit from driving against cost of accidents - Takes **efficient** activity level - Under strict liability, .blue[victim] does not bear cost of accidents - Ignores cost of accidents when deciding how much to bicycle - Takes **inefficiently high** activity level - .hi-purple[Strict liability leads to **efficient** level of injurer activity, **inefficiently high** level of victim activity] ] ] .pull-right[ .center[  ] ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | --- # Comparing Incentives Under Different Liability Rules .pull-left[ .smallest[ - So for both precaution & activity level: - .hi[No liability] leads to **inefficient** behavior by .red[injurer], **efficient** behavior by .blue[victim] - .hi[Strict liability] leads to **efficient** behavior by .red[injurer], **inefficient** behavior by .blue[victim] - Like the .hi-purple[paradox of compensation] from contract law! - One rule sets multiple incentives...we can't get them all right - ...or can we? Tort law has this One Weird Trick<sup>TM</sup> ] ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # Negligence --- # Negligence .pull-left[ - .hi[Negligence rule]: .red[Injurer] is only liable **if he breached his duty of due care** - Put alternatively, liable only if accident is “his fault” - Within our model: - Legal standard of care `\(x^l\)` - .red[Injurer] owes damages if `\(x < x^l\)` - If `\(x<x^l \rightarrow D=A\)` - If `\(x \geq x^l \rightarrow D=0\)` ] .pull-right[ .center[  ] ] --- # Negligence .pull-left[ - Private cost to .red[injurer] is: ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-13-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Negligence .pull-left[ - Private cost to .red[injurer] is: `$$\begin{cases} p(x)A+wx && \text{if } x<x^l\\ \end{cases}$$` ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-14-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Negligence .pull-left[ - Private cost to .red[injurer] is: `$$\begin{cases} p(x)A+wx && \text{if } x<x^l\\ wx && \text{if } x \geq x^l\\ \end{cases}$$` ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-15-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Negligence .pull-left[ - Private cost to .red[injurer] is: `$$\begin{cases} p(x)A+wx && \text{if } x<x^l\\ wx && \text{if } x \geq x^l\\ \end{cases}$$` - If standard of care `\(x^l\)` is set to `\(x^\star\)`, .red[injurer] minimizes private cost by taking efficient caution ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-16-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Negligence: Injurer Precaution .pull-left[ - What about .blue[victim]'s incentives? - We saw .red[injurer] will exercise due care and *not* be liable! - .blue[Victim] now bears cost of any accidents! (.hi-purple[residual risk]) - Private cost to .blue[victim] is: `\(\color{blue}{p(y)A+wy}\)` - .blue[Victim] chooses `\(y^\star\)`, efficient precaution too! ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-17-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | Negligence<sup>.magenta[†]</sup> | .green[Efficient] | .green[Efficient] | | | .footnote[<sup>.magenta[†]</sup> Assuming standard of care is set at the efficient level `\\((x^l=x^*)\\)`] --- class: inverse, center, middle # A Family of Negligence Rules --- # Other Negligence Rules .pull-left[ - The rule we just considered is “simple” negligence - Only consider .red[injurer]'s actions in determining liability - But in deciding whether .red[injurer] should be liable, we could also consider whether the .blue[victim] was negligent ] .pull-right[ .center[  ] ] --- # Contributory Negligence: Butterfield v. Forrester .pull-left[ .smallest[ - *Butterfield v. Forrester*, 11 East. 60, 103 Eng. Rep. 926 (K.B. 1809) - Forrester (Defendent) placed a pole in road next to his house while making repairs - Butterfield (Plaintiff) was riding at high speed at night, hit the pole, fell off his horse, sued for damages - Witness said that if Forrester had not been riding fast, would have seen the pole - Jury ruled Plaintiff should not be able to collect damages from Plaintiff due to their own .hi[contributory negligence] ] ] .pull-right[ .center[  ] .smallest[ > “One person being in fault will not dispense with another’s using ordinary care for himself.” ] ] --- # Injurer & Victim Negligence .pull-left[ - Let’s compare the whole family of negligence rules - .red[Injurer] is **negligent/at fault** when they fail to take due care, `\(x<x^*\)`<sup>.magenta[†]</sup> - .blue[Victim] is **negligent/at fault** when they fail to take due care, `\(y<y^*\)`<sup>.magenta[†]</sup> - Now let’s consider who is **liable** for the accident under various negligence rules .tiny[<sup>.magenta[†]</sup> Assuming standards of care are set at the efficient levels `\\(x^l=x^\star\\)` and `\\(y^l=y^\star\\)`] ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-18-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Simple Negligence .pull-left[ - **Simple negligence**: - .red[Injurer] is liable if they do not take due care `\(x<x^*\)` - .red[Injurer] is *not* liable if they *do* take due care `\(x \geq x^*\)` - .blue[Victim] cannot collect damages for any accident ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-19-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Negligence With a Defense of Contributory Negligence .pull-left[ - **Negligence with a defense of Contributory Negligence**: - .red[Injurer] is liable if they do not take due care `\(x<x^*\)` - .red[Injurer] is *not* liable if .blue[Victim] does not take due care `\(y<y^*\)` ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-20-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Comparative Negligence .pull-left[ - **Comparative Negligence**: if both parties are negligent, they share the cost of the accident (possibly proportionately) - e.g. if accident cause was 70% .red[injurer]’s fault, 30% .blue[victim]’s fault, .red[injurer] pays for 70% of damages ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-21-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Strict liability with Contributory Negligence .pull-left[ - **Strict liability with defense of Contributory Negligence**: - .red[Injurer] is liable (regardless of their level of precaution `\(x)\)` *unless* .blue[Victim] does not take due care `\(y<y^*\)` ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-22-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Family of Negligence Rules .pull-left[ <img src="4.2-slides_files/figure-html/unnamed-chunk-23-1.png" width="504" style="display: block; margin: auto;" /> <img src="4.2-slides_files/figure-html/unnamed-chunk-24-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ <img src="4.2-slides_files/figure-html/unnamed-chunk-25-1.png" width="504" style="display: block; margin: auto;" /> <img src="4.2-slides_files/figure-html/unnamed-chunk-26-1.png" width="504" style="display: block; margin: auto;" /> ] -- .smallest[ - These rules differ only in distribution of income - .hi-purple[Any of these rules (with efficient standard of care) incentivize efficient precaution by both parties!] `\((\color{blue}{x^\star}, \color{red}{y^\star})\)` ] --- class: inverse, center, middle # Comparing Negligence Rules, A Discrete Example of Bilateral Caution --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Let's compare with a discrete example - Each party .red[Injurer] and .blue[Victim] can either take **precaution** or **not** - Precaution costs each party $20 - Each accident costs $1,000 in harm - Chance of accident is: - 10% if nobody takes precaution - 6% if one party takes precaution - 2% if both parties take precaution - Note: precaution is efficient for each party: costs $20; reduces expected damage by 0.04($1,000) = $40 ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **negligence with defense of contributory negligence** - .red[Injurer] is liable if he failed to take precaution...unless .blue[blue] victim failed too ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **negligence with defense of contributory negligence** - .red[Injurer] is liable if he failed to take precaution...unless .blue[blue] victim failed too - Notice .blue[Victim]'s dominant strategy is **Precaution** - If .red[Injurer] not taking precaution, .blue[victim] wants to avoid liability - If .red[Injurer] takes precaution, .blue[victim] bears residual risk, wants to minimize accidents ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **negligence with defense of contributory negligence** - .red[Injurer] is liable if he failed to take precaution...unless .blue[blue] victim failed too - Notice .blue[Victim]'s dominant strategy is **Precaution** - If .red[Injurer] not taking precaution, .blue[victim] wants to avoid liability - If .red[Injurer] takes precaution, .blue[victim] bears residual risk, wants to minimize accidents - For .red[Injurer], best response to .blue[Victim]'s precaution is precaution - .hi-purple[Nash Eq.]: (.red[Precaution], .blue[precaution]), efficient! ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **comparative negligence**, cost of accident divided proportionately ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **comparative negligence**, cost of accident divided proportionately - Notice .blue[Victim]'s dominant strategy is **Precaution** ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **comparative negligence**, cost of accident divided proportionately - Notice .blue[Victim]'s dominant strategy is **Precaution** - For .red[Injurer], best response to .blue[Victim]'s precaution is precaution - .hi-purple[Nash Equilibrium]: (.red[Precaution], .blue[precaution]) and is efficient! ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **strict liability with defense of contributory negligence** - .red[Injurer] is liable regardless of his precaution ... unless .blue[blue] victim was negligent ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **strict liability with defense of contributory negligence** - .red[Injurer] is liable regardless of his precaution ... unless .blue[blue] victim was negligent - Notice .blue[Victim]'s dominant strategy is **Precaution** ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Discrete Example of Bilateral Precaution .pull-left[ .smallest[ - Consider rule of **strict liability with defense of contributory negligence** - .red[Injurer] is liable regardless of his precaution ... unless .blue[blue] victim was negligent - Notice .blue[Victim]'s dominant strategy is **Precaution** - For .red[Injurer], best response to .blue[Victim]'s precaution is precaution - .hi-purple[Nash Equilibrium]: (.red[Precaution], .blue[precaution]) and is efficient! ] ] .pull-right[ .center[  ] .quitesmall[ A: $1,000 w: $20 (each party) p: 10% (neither), 6% (one careful), 2% (both) ] ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | .green[Efficient] | | | | Negligence w/Contributory Negligence | .green[Efficient] | .green[Efficient] | | | | Comparative Negligence | .green[Efficient] | .green[Efficient] | | | | Strict Liability w/Contributory Negligence | .green[Efficient] | .green[Efficient] | | | Assuming all relevant standards of care are set at the efficient levels `\((x^l=x^*)\)` --- # Activity Levels under Negligence Rules .pull-left[ .smallest[ - **Simple negligence**: .red[injurer] liable if he was negligent - Leads .red[injurer] to take efficient precaution, so **injurer expects to not be liable for any accidents** - So .red[Injurer] ignores cost of accidents when deciding on activity level - Drives carefully, but still **drives too much** - .blue[Victim] bears residual risk - Bikes carefully, and bikes **efficient amount** ] ] .pull-right[ .center[  ] ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Negligence w/Contributory Negligence | .green[Efficient] | .green[Efficient] | | | | Comparative Negligence | .green[Efficient] | .green[Efficient] | | | | Strict Liability w/Contributory Negligence | .green[Efficient] | .green[Efficient] | | | Assuming all relevant standards of care are set at the efficient levels `\((x^l=x^*)\)` --- # Activity Levels under Negligence Rules .pull-left[ .smallest[ - **Contributory Negligence** and **Comparative negligence**: efficient precaution by both parties - Leads .red[injurer] to take efficient precaution, so **injurer expects to not be liable for any accidents** - So .red[Injurer] ignores cost of accidents when deciding on activity level - Drives carefully, but still **drives too much** - .blue[Victim] bears residual risk - Bikes carefully, and bikes **efficient amount** ] ] .pull-right[ .center[  ] ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Negligence w/Contributory Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Comparative Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Strict Liability w/Contributory Negligence | .green[Efficient] | .green[Efficient] | | | Assuming all relevant standards of care are set at the efficient levels `\((x^l=x^*)\)` --- # Activity Levels under Negligence Rules .pull-left[ .smallest[ - **Strict liability w/comparative negligence defense**: if .blue[victim] is not negligent, .red[injurer] is liable regardless of precaution - Leads both parties to take efficient precaution, so .red[injurer] is residual risk bearer, and is **liable for any accidents** - So .red[injurer] weighs cost of accidents against benefits, drives **efficient amount** - .blue[Victim], fully insured, ignores cost of accidents when deciding on activity level - Bikes carefully, but still **bikes too much** ] ] .pull-right[ .center[  ] ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Negligence w/Contributory Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Comparative Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Strict Liability w/Contributory Negligence | .green[Efficient] | .green[Efficient] | .green[Efficient] | Too High | Assuming all relevant standards of care are set at the efficient levels `\((x^l=x^*)\)` --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .b[.ul[.green[Efficient]]] | .green[Efficient] | .b[.ul[Too High]] | .green[Efficient] | | Negligence w/Contributory Negligence | .b[.ul[.green[Efficient]]] | .green[Efficient] | .b[.ul[Too High]] | .green[Efficient] | | Comparative Negligence | .b[.ul[.green[Efficient]]] | .green[Efficient] | .b[.ul[Too High]] | .green[Efficient] | | Strict Liability w/Contributory Negligence | .green[Efficient] | .b[.ul[.green[Efficient]]] | .green[Efficient] | .b[.ul[Too High]] | .smallest[ Highlighted cases: party takes precaution only to AVOID liability `\(\implies\)` precaution is efficient, but activity level is too high ] --- # Comparing Incentives Under Different Liability Rules | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .b[.ul[.green[Efficient]]] | Too High | .b[.ul[.green[Efficient]]] | | Strict liability | .b[.ul[.green[Efficient]]] | Zero | .b[.ul[.green[Efficient]]] | Too High | | (“Simple”) Negligence | .green[Efficient] | .b[.ul[.green[Efficient]]] | Too High | .b[.ul[.green[Efficient]]] | | Negligence w/Contributory Negligence | .green[Efficient] | .b[.ul[.green[Efficient]]] | Too High | .b[.ul[.green[Efficient]]] | | Comparative Negligence | .green[Efficient] | .b[.ul[.green[Efficient]]] | Too High | .b[.ul[.green[Efficient]]] | | Strict Liability w/Contributory Negligence | .b[.ul[.green[Efficient]]] | .green[Efficient] | .b[.ul[.green[Efficient]]] | Too High | .smallest[ Highlighted cases: party reduces accidents, since they bear the cost, so both precaution & activity level are both efficient ] --- # These Results Look Overwhelming | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Negligence w/Contributory Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Comparative Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Strict Liability w/Contributory Negligence | .green[Efficient] | .green[Efficient] | .green[Efficient] | Too High | These results look overwhelming, but really the result of four basic ideas --- # These Results Look Overwhelming | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | | Too High | | | Strict liability | | Zero | | Too High | | (“Simple”) Negligence | | | | | | Negligence w/Contributory Negligence | | | | | | Comparative Negligence | | | | | | Strict Liability w/Contributory Negligence | | | | | 1) If you don’t bear any of the cost of accidents, you have no incentive to prevent them --- # These Results Look Overwhelming | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | | | | | | Negligence w/Contributory Negligence | | | | | | Comparative Negligence | | | | | | Strict Liability w/Contributory Negligence | | | | | 2) If you **do** bear the cost of accidents, you’ll do whatever you can to prevent them --- # These Results Look Overwhelming | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | | Too High | | | Negligence w/Contributory Negligence | .green[Efficient] | | Too High | | | Comparative Negligence |.green[Efficient] | | Too High | | | Strict Liability w/Contributory Negligence | | .green[Efficient] | | Too High | 3) If you can avoid liability by exercising due care, you’ll do it, but then you won’t reduce activity --- # These Results Look Overwhelming | Rule | .red[Injurer] Precaution | .blue[Victim] Precaution | .red[Injurer] Activity | .blue[Victim] Activity | |------|---------|--------|-----|-----| | No liability | Zero | .green[Efficient] | Too High | .green[Efficient] | | Strict liability | .green[Efficient] | Zero | .green[Efficient] | Too High | | (“Simple”) Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Negligence w/Contributory Negligence | .green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Comparative Negligence |.green[Efficient] | .green[Efficient] | Too High | .green[Efficient] | | Strict Liability w/Contributory Negligence | .green[Efficient] | .green[Efficient] | .green[Efficient] | Too High | 4) If the other guy can duck liability with due care, you’re the residual risk bearer, and therefore you’ll take due care